The environmental opportunity in special and hazardous waste management

Environmental problem

Europe generates around 2.5 billion tonnes of waste annualy, equivalent to the mass of around 385 Great Pyramids of Cheops.

Europe generates an enormous volume of waste each year, around 2.5 billion tonnes. Approximately 90% originates from economic activities and is generally classified as industrial waste, while household waste’ accounts only for the remaining 10%.

Of the 2.2 billion tonnes of industrial waste generated annually, roughly 120 million tons are hazardous - meaning they pose a risk to human health or the environment. Although these waste streams represent a relatively small share of total volumes, they account for a disproportionate level of environmental risk, complexity and regulatory scrutiny.

Figure 1. European waste production 2022, by volume

Along the waste management value chain, five fundamental challenges shape both environmental outcomes and market dynamics. These challenges are interconnected and often reinforce one another.

Hazardous waste accounts for only ~5% of industrial volumes, yet drives a disproportionate share of risk, cost, and complexity.

1. Industrial waste generation remains structurally resilient

Industrial waste generation has historically remained closely linked to industrial production and has proven highly resilient, particularly in major European economies such as Italy, Germany and France. At the broader European level, slightly weaker trends mainly reflect country-specific factors, such as the decline in mining activity in Greece in 2020. This resilience underscores a persistent environmental challenge, as significant reductions in waste volumes remain unlikely despite circular economy initiatives and increasing levels of on-site reuse and recovery. From a market perspective, waste management turnover across both industrial and municipal waste streams has grown at a CAGR of approximately 4% over the past five years, broadly in line with GDP growth and supported by treatment and disposal capacity constraints.

Figure 2. Waste generation and sector turnover correlate with industrial production and GDP

2. Waste classification remains a critical challenge

Waste can enter the management chain incorrectly classified, leading to inappropriate storage, handling and transport. This increases the risk of hazardous and non-hazardous streams being mixed, raising environmental risks such as spills, soil contamination and groundwater pollution, while reducing the effectiveness of downstream treatment and recovery processes.

3. Recovery rates remain constrained for complex waste streams

Industrial and hazardous waste streams often face significant technological and economic barriers to recovery. As a result, recovery rates remain limited at around 40–45%, with a substantial share of waste still directed to disposal rather than material recovery, restricting progress towards circularity.

Recovery rates for complex waste streams remain capped at just 40-45%, leaving significant value unrealised.

4. Treatment capacity is unevenly distributed across Europe

Treatment infrastructure is concentrated in a small number of countries, particularly Germany, Sweden and Finland, while structural capacity shortages persist in markets such as Italy and Belgium. This imbalance, combined with slower infrastructure development due to public opposition and regulatory delays, creates bottlenecks in waste routing and limits recovery opportunities.

5. Cross-border shipments remain essential to the system

Capacity constraints and regulatory requirements create a structural need for cross-border waste shipments, with around 10% of Europe's hazardous waste transported internationally for treatment. While this enables access to specialised facilities, it also increases costs, operational complexity and dependence on external markets. For example, Italy is a major exporter of hazardous waste streams such as contaminated soils and lead batteries, while Germany is a key importer. As a result, waste generated in southern Italy may be transported to northern Germany for treatment or disposal, shifting value creation away from the point of origin and increasing costs for waste producers.

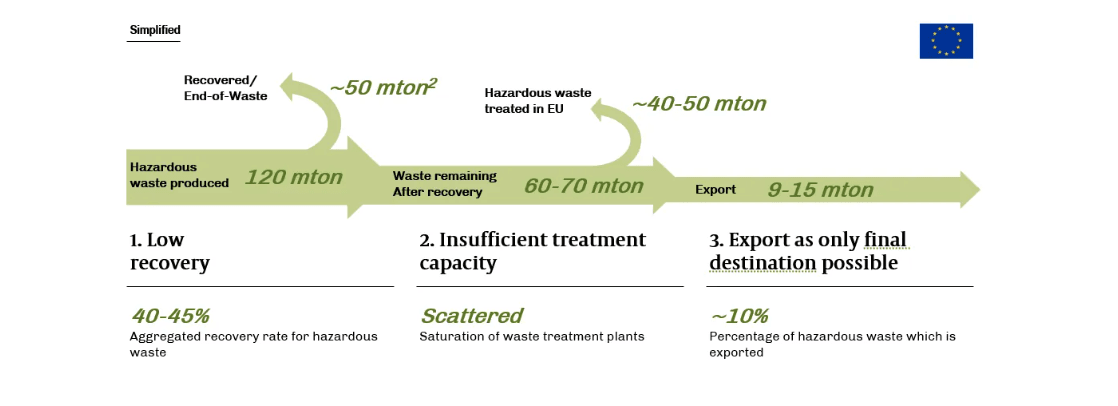

Figure 3. Hazardous waste recovery rates in Europe remain limited at 40–45%, with approximately 10% of volumes exported to access suitable treatment capacity.

Environmental solutions along the value chain

Managing special and hazardous waste involves a chain of specialised activities, each reducing environmental risk in different ways. Addressing the structural issues therefore requires coordinated action across four main actors along the value chain.

Figure 4. Waste management value chain

- Waste producers reduce waste at the source, implementing circular economy and waste reduction practices.

- Brokers enhance traceability and routing efficiency through proper auditing, documentation, tracking and coordination, mitigating the risk of mismanagement and ensuring that waste is directed toward appropriate downstream solutions.

- Pre-treatment platforms enhance recovery rates and cost efficiency by aggregating, safely storing, sorting, and repackaging waste, as well as performing initial physico-chemical treatments. They play a critical role in reducing downstream rejection, lowering logistics and gate fees, and increasing the likelihood of recovery over disposal. For example, operators might optimise the blend of hazardous waste streams (e.g. dry solids and liquid waste) to achieve a stable feedstock with higher calorific value to be sent to waste-to-energy.

- Treatment facilities ultimately control whether waste is recovered or disposed of, as waste to energy or in landfill. As a result, treatment capacity is critical to environmental outcomes: if it is scarce, fragmented, or poorly located, even well-managed upstream waste may travel long distances or be diverted to lower-value disposal options.

Both brokers and dealers (pre-treatment platform) are often overlooked when assessing their contribution to sustainable impact, and are frequently perceived as simple intermediaries within the value chain. This greatly underestimates their critical role in enabling efficient waste management, and fails to give enough credit to players which are crucial to addressing the complexities of mixed waste streams and material recovery. Their role is particularly important for waste producers that often lack both the operational focus on waste management and the specialised expertise required to manage these challenges effectively.

Investment opportunities

The complexity of waste streams and value chain activities leads to diverse business models, often combining multiple revenue and margin drivers within the same company.

Certain waste streams have positive intrinsic value, where operators acquire waste and generate revenue through the sale of recovered outputs such as metals or electronic components. . In contrast, hazardous and complex waste streams typically have negative value, requiring operators to be paid for their safe handling and management, in addition to incurring costs for final disposal. In these cases, revenues are primarily driven by gate fees, with margins structurally supported by regulatory barriers and constrained treatment capacity.

The competitive landscape varies across Europe. More consolidated markets like France and the UK are dominated by large integrated players such as Veolia, Suez and Biffa, while countries such as Italy and Germany remain highly fragmented, especially in collection and intermediation.

This structural complexity also underpins an attractive investment landscape within a European market valued at approximately €260 billion and growing at around 4% CAGR. Value accrues unevenly along the chain: upstream activities are fragmented and service-driven, pre-treatment platforms gain operational leverage, and treatment assets capture the highest scarcity-driven value. This is reflected in margin profiles, with approximately 10–20% EBITDA for brokers, 15–25% for pre-treatment platforms and 20–30%+ for treatment assets, highlighting the increasing defensibility of infrastructure-backed activities.

Against this backdrop, multiple investment opportunities emerge, depending on the degree of fragmentation, regulatory complexity, and asset intensity of each value segment. More fragmented and service-oriented niches, such as brokerage, collection, and selected pre-treatment activities, are often well suited to buy-and-build strategies, allowing players to expand geographic coverage, broaden service offerings, and strengthen customer relationships through scale. In contrast, more specialised treatment and recovery activities, including solvent recovery or waste-to-energy plants, typically benefit from higher barriers to entry, including permitting requirements, technical expertise, and infrastructure scarcity. These characteristics support stronger competitive positioning, greater pricing power and more defensive, infrastructure-like business models.

Closing thoughts

Special and hazardous waste management is a mission-critical environmental infrastructure that determines whether complex waste streams are traced, recovered and treated safely, or instead become a source of pollution, inefficient disposal and cross-border dependence.

Environmental and investment value align around critical infrastructure control.

The opportunity lies in shifting from basic waste handling towards integrated platforms and assets that make the system more traceable, more circular and more self-sufficient. Environmental and investment value increasingly converge on a single scarce resource: access to and control of critical waste infrastructure.

Important information

This material is of a promotional nature and is provided for information purposes only. Please note that this material may contain technical language. For this reason, they may not be suitable for readers without professional investment experience. This document is issued by Ambienta SGR S.p.A. It is not intended for solicitation or for an offer to buy or sell any financial instrument, distribution, publication, or use in any jurisdiction where such solicitation, offer, distribution, publication or use would be unlawful, nor is it aimed at any person or entity to whom it would be unlawful to address such a document.

This material is of a promotional nature and is provided for information purposes only. Please note that this material may contain technical language. For this reason, they may not be suitable for readers without professional investment experience. This document is issued by Ambienta SGR S.p.A. It is not intended for solicitation or for an offer to buy or sell any financial instrument, distribution, publication, or use in any jurisdiction where such solicitation, offer, distribution, publication or use would be unlawful, nor is it aimed at any person or entity to whom it would be unlawful to address such a document.

Nothing in this document constitutes legal, accounting or tax advice. The information and analysis contained herein are based on sources considered reliable. Ambienta SGR S.p.A uses its best effort to ensure the timeliness, accuracy, and comprehensiveness of the information contained in this marketing communication. Nevertheless, all information and opinions as well as calculations indicated herein may change without notice.

Ambienta SGR S.p.A. has not considered the suitability of this investment against your individual needs and risk tolerance. To ensure you understand whether our product is suitable, please read the Prospectus and relevant offering documents. Any decision to invest must be based solely on the information contained in the Prospectus and the offering documentation. We strongly recommend that you seek independent professional advice prior to investing.