The Petrochemical Industry

Introduction

Petrochemicals make up ~15% of global oil demand, potentially rising to 30% by 2050.

Petrochemicals are chemical products derived primarily from petroleum. The two main groups, olefins and aromatics, serve as the building blocks for a wide range of materials, including plastics, resins, fibres, solvents, detergents and adhesives. Though largely invisible, these molecules underpin the modern economy, appearing in around 95% of manufactured goods, from packaging and textiles to vehicles and buildings. Today, petrochemicals account for roughly 15% of global oil demand.

As transport electrification reduces demand for fuel, petrochemicals are expected to take a larger share of oil use, potentially rising to around 30% by 2050. Demand has proven resilient, growing steadily at 3 to 4% per year over the past decade. Polymers, including plastics and synthetic fibres, make up more than 70% of this demand and remain the sector’s main growth driver. The rest is spread across applications such as detergents, solvents, tyres and rubber products.

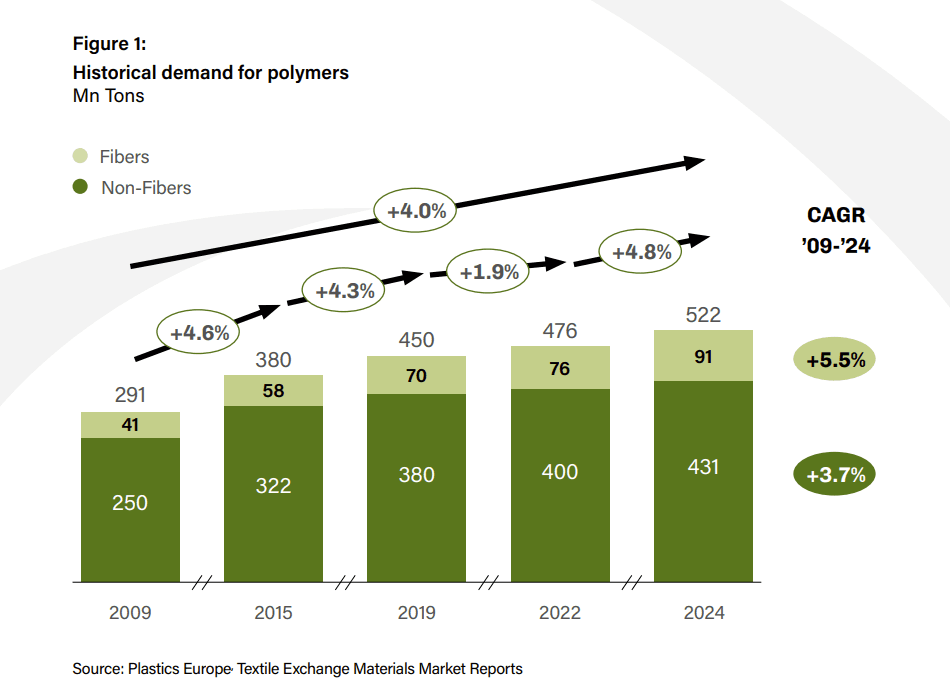

Despite sustained public and political scrutiny, there is little evidence of largescale substitution away from plastics. Global polymer production reached around 520 million tonnes in 2024, reflecting a steady 4% annual growth rate over the past 15 years (Fig. 1). This includes roughly 90 million tonnes of synthetic fibres, often excluded from conventional plastic statistics, but a major source of demand. Synthetic fibres alone have grown by about 5% annually over the past decade, accelerating to around 10% since 2022.

Efforts to curb plastic use, particularly in packaging, have yet to shift overall demand. Alternatives have not scaled sufficiently, and end use demand remains strong across packaging, textiles, construction and transport. Polyester continues to gain share in textiles, plastics remain dominant in food and beverage packaging, and construction materials still rely heavily on polymer products. In transport, electrification can even increase plastic use through batteries and electrical systems.

Until very recently, the cost advantage of virgin polymers has strengthened, supported by low oil prices and structural overcapacity driven by expansion in China and the Middle East. This has made alternatives less competitive. However, recent disruptions such as the Iran crisis may begin to shift this balance, improving the relative attractiveness of more sustainable solutions while also highlighting the importance of supply security.

As a half trillion-dollar industry, petrochemicals are central to the future of material sustainability. Their evolution is closely tied to oil market dynamics, geopolitics and shifting supply chains. Production of key building blocks is rapidly relocating, with new capacity concentrated in China, the United States and the Middle East, and increasing use of gas and coal-based feedstocks. Europe, by contrast, faces structural disadvantages, with an estimated 20 to 30% of its ethylene capacity expected to close by 2027.

Environmental problem

Between 10 and 40 million tons of microplastics enter the environment annually.

Petrochemicals are not inherently and always harmful to the environment, and in many cases the benefits of their use can far outweigh the environmental burden of producing them. For example, thermal insulation of buildings, where the lifetime benefits of reducing building heating demand far outweigh the cost of making the material. However, this is not always the case, and the petrochemical industry does face several environmental challenges, which can be clustered into four categories:

- Non-renewable nature: Starting from raw materials, the industry is almost entirely reliant on nonrenewable fossil feedstocks, primarily oil but increasingly also gas and coal, the fastest growing raw materials in the petrochemical industry.

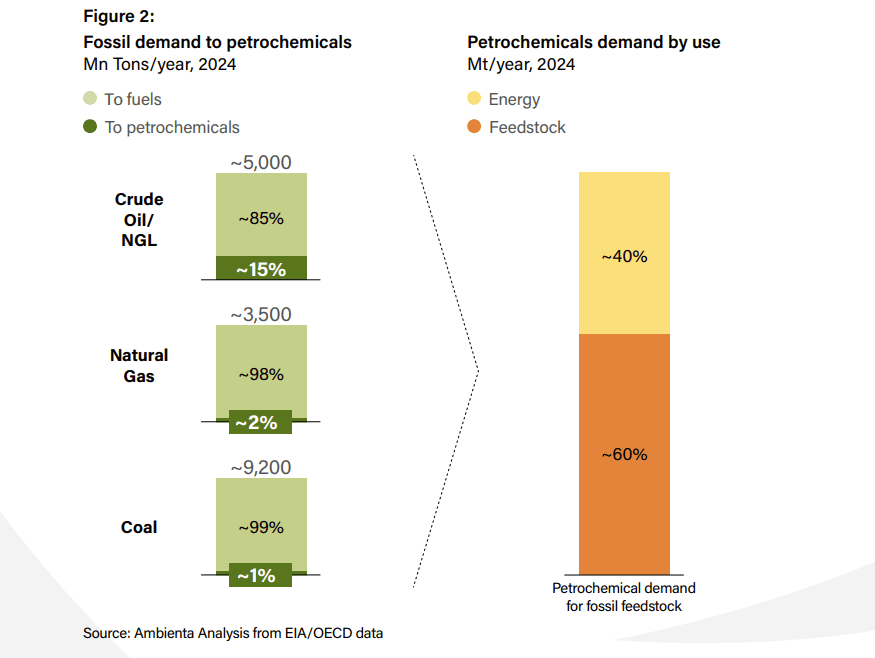

- Process emissions: At a sector level, 40-50% of the fossil inputs of petrochemical processes are burned to provide the necessary energy, mostly in the form of heat (Fig. 2). Steam cracking, the core petrochemical process that breaks down hydrocarbon feedstock into smaller, more useful molecules, takes place at temperatures of 800°- 900°C, representing the bulk of energy demand and of process CO2 emissions. For example, for each ton of ethylene, one of the main chemical building blocks, the steam cracker alone emits 1-2 tons of CO2 .

Globally, less than 10% of plastics are produced from recycled materials.

- Pollution: Probably the least understood and invisible environmental impact, but also potentially the most consequential. During their use phase, many petrochemical products release fragments into the environment; common examples include tire wear on roads, the weathering of paint, and the shedding of synthetic fibers during laundering. These fragments, generally defined as “microplastic”, are today ubiquitous: they have been detected in many bottled-water samples and can happen also with food-contact plastic packaging, especially under certain use conditions such as heating, abrasion, or repeated use. It is estimated that between 10 and 40 million tons of microplastics enter the environment annually, accumulating in water, soil, and living organisms. There is growing scientific evidence of the health risks from microplastics in humans, including endocrine disruption and inflammatory responses, with publications on this topic doubling between 2019 and 2025. Nonetheless, these are insufficient for conclusive sizing of these risks and subsequent regulatory action. For some additives, on the other hand, over the years research has become more conclusive, leading to restrictions and bans. BPA plasticisers for instance were banned from food contact materials by the European Commission in 2024.

- End-of-life management: While in high-income countries plastic waste is mostly collected and leakage is limited to littering. In contrast, middle- and low-income countries face much greater challenges: an estimated 40–60% of plastic waste is either openly burned or leaks into the environment. Even when waste is collected, landfill and incineration remain the dominant treatment methods. Globally, less than 10% of plastics are made from recycled materials. As energy grids become cleaner due to increasing renewable penetration, the relative impact of burning plastic in “waste-to-energy” plants becomes more significant. These facilities can produce CO₂ emissions that are 2–4 times higher than the average European grid emission factor. This raises important questions about their role as a sustainable waste management solution.

Environmental solutions

The most commercially mature decarbonisation lever in petrochemicals today is electrification of low- and medium-temperature process heat.

Addressing the four key environmental challenges of petrochemicals requires action across four main solution areas: transitioning to renewable feedstocks, reducing process emissions, adopting alternative materials, and improving end-oflife management.

While progress is being made in each of these areas, all pathways face significant barriers related to cost, scalability, and technical feasibility. As a result, despite these advances, they remain collectively insufficient to fully steer the industry toward a comprehensive global solution.

- Renewable feedstocks: Most of the chemical building blocks used in the industry are, in essence, chains of carbon and hydrogen molecules. They do not necessarily need to come from hydrocarbons, and all building blocks can be produced using different pathways.

One route is biological: biomass, agricultural residues, used cooking oils, animal fats and other bio-based feedstocks can be converted into intermediates such as bio-naphtha, paraffinic streams or syngas, which can then enter conventional petrochemical units as drop-in inputs. This is already happening at small but growing scale. Bio-naphtha is particularly important because it can be used directly in existing steam crackers with limited asset changes, making it one of the most practical low-carbon feedstock options available today. However, volumes remain small and prices are typically around three times that of fossil naphtha, making it unviable for bulk commodity chemicals. In selected specialty chemical niches, such as surfactants and detergents, bio-based alternatives are gaining traction (See Ambienta’s Lens on Bio-based chemicals and our recent Theme of the Month focused on Fermentation), especially when novel production processes improve yields, reduce energy intensity or simplify downstream processes. Another route is electrochemical: electricity can be used to electrolyse water and produce hydrogen, which can then be combined with CO2 to produce methanol or syngas-derived hydrocarbons. These can in turn be converted into olefins and other petrochemical building blocks. This pathway is conceptually attractive because it decouples the sector from fossil feedstocks, but again it remains far from cost parity looking at recent cost estimates of green hydrogen production, and requires ample, stable supply of renewable power. Similarly to the biobased case, cost competitiveness requires further process innovation. A third option is to use waste as a feedstock, which we cover in more detail in the subsequent end-of-life management section.

Another route is electrochemical: electricity can be used to electrolyse water and produce hydrogen, which can then be combined with CO2 to produce methanol or syngas-derived hydrocarbons. These can in turn be converted into olefins and other petrochemical building blocks. This pathway is conceptually attractive because it decouples the sector from fossil feedstocks, but again it remains far from cost parity looking at recent cost estimates of green hydrogen production, and requires ample, stable supply of renewable power. Similarly to the biobased case, cost competitiveness requires further process innovation.

A third option is to use waste as a feedstock, which we cover in more detail in the subsequent end-of-life management section. - Reducing process emissions: The most commercially mature decarbonisation lever in petrochemicals today is electrification of low- and mediumtemperature process heat. Industrial heat pumps generating steam at 150–200°C are already proven and cost-competitive in many European facilities, leveraging the abundant waste heat generated in chemical plants. Adoption is accelerating and elevated natural gas prices reinforce the business case.

The bigger challenge is the electrified steam cracker. In 2024 the world’s first large-scale demonstration of an electrically heated cracker furnace was built at BASF’s Ludwigshafen site. Early results indicate that direct furnace emissions can be cut by 95% or more when powered by renewable electricity. The e-furnace design can be retrofitted to existing crackers, which reduces the capital barrier relative to greenfield build. Other initiatives are also emerging, including the European Cracker of the Future consortium and a solution by Finnish company Coolbrook. Its Rotodynamic Reactor uses electric motors to generate heat directly within the feedstock, eliminating the need for a conventional furnace altogether.

Scaling constraints remain substantial and should not be underestimated. A single commercial-scale cracker furnace requires hundreds of megawatts of power. To deliver meaningful emission reductions, this electricity must be low-carbon, yet it cannot rely solely on variable renewables given the need for continuous operation.

In the near term, the most realistic pathway is partial electrification of existing crackers, replacing only a subset of furnaces. Fully electrified, commercial-scale crackers are unlikely to be deployed before 2030–2035. - Alternative materials: Alternative materials are often presented as the obvious answer to petrochemical dependence, but the reality is more complex. Whether paper, glass, aluminum, wood, reusable systems or bio-based materials are environmentally preferable depends heavily on the specific application, transport intensity, reuse rates, contamination risk and endof-life infrastructure. In some niches, alternatives clearly outperform plastics; in others, they simply shift environmental burdens from fossil carbon to weight, energy use, land use or cost. At the macro level, no alternative material has yet scaled sufficiently to alter global polymer demand trajectories. Material substitution is therefore likely to remain selective and application-specific rather than the primary solution to petrochemical growth.

.jpg&w=3840&q=80)

The most effective end-of-life solutions are those that also address the feedstock challenge.

- Improving end-of-life management: The most effective end-of-life solutions are those that also address the feedstock challenge. In principle, waste plastics, tires, and several other waste streams can be converted into polymers, naphtha, methanol, or monomers that feed back into petrochemical production, thereby displacing some demand for virgin fossil inputs. This approach is strategically attractive because it tackles both circularity and fossil dependence at the same time.

However, achieving this in practice requires a mix of different pathways, each with distinct economics and environmental outcomes.

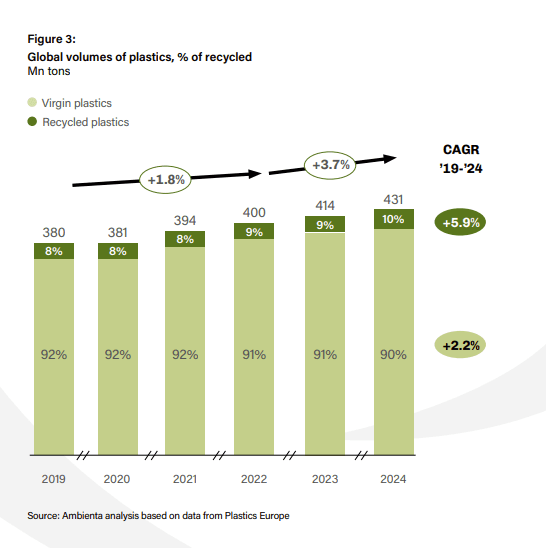

- Mechanical recycling (shredding, washing and re-pelletising) remains the most environmentally and economically sound route where applicable. It preserves material value with relatively limited processing, and its carbon footprint can be a fraction of both incineration and virgin plastic production. The main constraints are output quality, which depends heavily on collection and sorting infrastructure, and economics: when virgin polymers are cheap as they have been in the past couple of years, mechanical recycling often requires mandates. (Fig. 3).

- Chemical recycling covers technologies that convert plastic waste back into usable chemical feedstocks or monomers. This includes pyrolysis and depolymerisation and can also include gasification when the resulting syngas is used to make new chemicals rather than power. It can handle a broader range of contaminated or mixed plastics unsuitable for mechanical processing, which makes it a complementary rather than alternative solution, and produces recycled feedstocks such as pyrolysis oil or recycled naphtha that can re-enter the petrochemical system as is, blended with oil-based naphtha. However, volumes remain very small relative to total plastics demand: announced capacity is roughly 5 Mt by 2030, still less than 1% of global plastic feedstock demand. Economics remain difficult, and environmental performance varies materially by technology and system boundary, with some cases exceeding the impacts of virgin materials, and therefore need to be carefully evaluated.

- Incineration with energy recovery remains widespread because it is operationally simple and significantly reduces waste volume. However, from a climate perspective, it is a weak solution. Burning plastic releases fossil carbon immediately, and the resulting emissions intensity can be substantially higher than that of grid electricity, typically around 2 to 4 times higher in Europe. In other words, while waste to energy may address a disposal challenge, it does little to advance either circularity or decarbonisation.

Investment opportunities

In bulk petrochemicals, most sustainable alternatives still struggle to compete with fossil routes on cost. Real disruption will require major process breakthroughs, not just feedstock substitution, and in some cases progress in adjacent technologies. Electrified steam crackers, for example, are limited not only by furnace design but also by the need for large amounts of reliable, low carbon baseload power.

There are, however, clearer opportunities for environmental investment across the value chain. Industrial heat electrification, particularly heat pumps for low and medium temperature processes, is already proven and becoming cost competitive. Mechanical recycling is another area of interest, especially the enabling steps such as sorting, washing, decontamination, compounding and quality control, which determine the quality and economics of recycled resin. While low virgin resin prices have slowed investment, regulation and supply security concerns are likely to revive momentum.

Selected bio-based niches also offer potential. While renewable feedstocks are expensive to scale in commodity chemicals, they can already be competitive in certain specialties and intermediates where process innovation improves yields and reduces energy use.

Downstream, the most compelling applications are those where product benefits outweigh material impacts. Building insulation stands out, as lifetime energy savings can far exceed the footprint of the polymer used.

Important information

This material is of a promotional nature and is provided for information purposes only. Please note that this material may contain technical language. For this reason, they may not be suitable for readers without professional investment experience. This document is issued by Ambienta SGR S.p.A. It is not intended for solicitation or for an offer to buy or sell any financial instrument, distribution, publication, or use in any jurisdiction where such solicitation, offer, distribution, publication or use would be unlawful, nor is it aimed at any person or entity to whom it would be unlawful to address such a document.

This material is of a promotional nature and is provided for information purposes only. Please note that this material may contain technical language. For this reason, they may not be suitable for readers without professional investment experience. This document is issued by Ambienta SGR S.p.A. It is not intended for solicitation or for an offer to buy or sell any financial instrument, distribution, publication, or use in any jurisdiction where such solicitation, offer, distribution, publication or use would be unlawful, nor is it aimed at any person or entity to whom it would be unlawful to address such a document.

Nothing in this document constitutes legal, accounting or tax advice. The information and analysis contained herein are based on sources considered reliable. Ambienta SGR S.p.A uses its best effort to ensure the timeliness, accuracy, and comprehensiveness of the information contained in this marketing communication. Nevertheless, all information and opinions as well as calculations indicated herein may change without notice.

Ambienta SGR S.p.A. has not considered the suitability of this investment against your individual needs and risk tolerance. To ensure you understand whether our product is suitable, please read the Prospectus and relevant offering documents. Any decision to invest must be based solely on the information contained in the Prospectus and the offering documentation. We strongly recommend that you seek independent professional advice prior to investing.